What happened at Alameda Research

If you want to read a poorly researched fluff piece about Sam Bankman-Fried, feel free to go to the New York Times (PDF). If you want to understand what happened at Alameda Research and how Sam Bankman-Fried (SBF), Sam Trabucco, and Caroline Ellison incinerated over $20 billion dollars of fund profits and FTX user deposits, read this article. (And follow me on Twitter at @0xfbifemboy!)

To be clear, we still don’t have a perfect understanding of what exactly happened at Alameda Research and FTX. However, at this point, I feel that we have enough information to get a grasp on the broad strokes. Through a combination of Twitter users’ investigations, forum anecdotes, and official news releases, the history of these two intertwined companies becomes progressively less hazy, slowly coalescing into something resembling a consistent narrative.

Of course, without witness testimonies and a full financial investigation, our claims only remain tentative at best. Any given piece of information may be flawed or even fabricated. However, if they are assembled together and put in context, they together lend credence to the following timeline:

- SBF, Trabucco, and Caroline were (probably) initially well-intentioned but not especially competent at running a trading firm

- Alameda Research made large amounts of book profits via leveraged longs and illiquid equity deals in the 2020-2021 bull market

- Although Alameda was likely initially profitable as a market maker, their edge eventually degraded and their systems became unprofitable

- Despite success with some discretionary positions, on net, Alameda & FTX jointly continued to lose large amounts of money and liquid cash throughout 2021-2022 as a result of excessive discretionary spending, illiquid venture investments, uncompetitive market-making strategies, risky lending practices, lackluster internal accounting, and general deficiencies in overall organizational ability

- When loans were recalled in early 2022, an emergency decision was made to use FTX users’ deposits to repay creditors

- This repayment spurred on increasingly erratic behavior and unprofitable gambling, eventually resulting in total insolvency

Details follow below. (Many thanks to all those who have contributed to this article, be it through private discussions or through public content that I’ve quoted or otherwise relied upon.)

Alameda Research probably lost >$15 billion dollars

To understand the FTX bankruptcy, we have to first understand the scope of the problem at hand. Most news accounts seem to portray the scale of the bankruptcy as relatively small. For example, the New York Times suggests that user deposits were used to make up for money that had gone into venture investments:

Meanwhile, at a meeting with Alameda employees on Wednesday, Ms. Ellison explained what had caused the collapse, according to a person familiar with the matter. Her voice shaking, she apologized, saying she had let the group down. Over recent months, she said, Alameda had taken out loans and used the money to make venture capital investments, among other expenditures.

Around the time the crypto market crashed this spring, Ms. Ellison explained, lenders moved to recall those loans, the person familiar with the meeting said. But the funds that Alameda had spent were no longer easily available, so the company used FTX customer funds to make the payments. Besides her and Mr. Bankman-Fried, she said, two other people knew about the arrangement: Mr. Singh and Mr. Wang.

Similarly, Matt Levine’s column seems to imply that the drop in the value of FTT used as collateral resulted in an enormous imbalance between assets and liabilities:

Now let’s add one more crypto element. If you are a crypto exchange, you might issue your own crypto token. FTX issues a token called FTT. The attributes of this token are, like, it entitles you to some discounts and stuff, but the main attribute is that FTX periodically uses a portion of its profits to buy back FTT tokens. This makes FTT kind of like stock in FTX: The higher FTX’s profits are, the higher the price of FTT will be. It is not actually stock in FTX — in fact FTX is a company and has stock and venture capitalists bought it, etc. — but it is a lot like stock in FTX. FTT is a bet on FTX’s future profits.

But it is also a crypto token, which means that a customer can come to you and post $100 worth of FTT as collateral and borrow $50 worth of Bitcoin, or dollars, or whatever, against that collateral, just as they would with any other token. Or something; you might set the margin requirements higher or lower, letting customers borrow 25% or 50% or 95% of the value of their FTT token collateral.

Both of these accounts miss a crucial part of the story. First, FTX is missing about $8 billion dollars’ worth of users’ collateral. Even if you consider the sum total of venture investments made by FTX and Alameda together, as well as a marginal drop in collateral value as a result of an FTT price decline, it simply does not make sense for FTX to be $8b in debt. The losses would be significant, yes, but they alone do not constitute a sufficient explanation for FTX’s bankruptcy.

In addition to that, it was popularly believed that FTX and Alameda together were enormously profitable, as a result of:

- High trading fees on FTX combined with large user trading volumes

- Extremely lucrative (or, depending on your perspective, predatory) venture deals for tokens such as SOL, MAPS, OXY, SRM, etc.

- Highly probable collusion between Alameda and FTX to give Alameda an edge over other market makers on FTX

Although it is difficult to put an exact dollar value to their estimated profits, it was believed that these avenues, especially the lucrative venture deals, were responsible for at least $10b in profit between Alameda and FTX combined.

We are therefore left with an even greater mystery. Somehow, it seems as though Alameda and FTX managed to burn through >$15 billion dollars’ worth of profits (likely more). This is an incredible shortfall, and, remarkably, no comprehensive account to date has emerged showing exactly how this came about!

We may never really know where all of the money went. However, we provide a number of separate hypotheses which, if combined together, could plausibly account for losses of $15 billion or more.

Alameda’s market-making edge decayed and they started punting longs

There has typically been a perception of Alameda as an extremely competent and profitable market maker. But is this perception actually accurate?

First of all, it’s worth noting that although the inner circle’s backgrounds (SBF and Caroline from Jane Street, Trabucco from SIG) are impressive, they are not exceptional. Having several years’ worth of experience at a trading firm does not make you a geniusーthe top tier of such firms hires well over a hundred new employees every year. In a podcast from 2019, SBF brags about making predictions on the timescale of 1-2 seconds:

Sam: Yes. A lot of exchanges have, if nothing else, volume-based features, and often we can get in the top tier there, and that does help a fair bit, especially when it comes to eeking out a business plan. […] That’s nothing. You made one basis point. If you guess randomly, maybe moderately right, about what Bitcoin is going to do in the next two seconds, maybe you make a basis point. [00:22:30] But if you can actually do that on one billion dollars a day of volume, then you can do the math, that’s actually a lot of money. We can’t always do that, but it sort of does mean that at some volume scale, you really do get down to, everything matters. Every little edge matters. So there is some of that. A lot of exchanges reach out to us about being liquidity fighters. We do do that on some exchanges.

While this might have been considered highly competitive in 2019-era crypto markets, it is a far cry from the microsecond-level precision of market making in traditional finance. (N.B.: Typically microsecond-level precision refers to a slightly different concept; however, even prediction of directional price movement takes place at timescales much lower than two seconds!) Such strategies may have served well three years ago, but as larger, extremely competent, and well capitalized market makers like Tower and XTX began to trade cryptocurrency markets, it is plausible that Alameda slowly lost its edge, much as Doug Colkitt suggests.

What do you do when:

- You start losing your edge as market maker despite all the hard work you put into writing complicated code, and

- Everyone around you is printing generational fortunes (at least on paper) by longing absolute dogshit?

Your natural inclination, of course, is to neglect your market-making activities and join the punters.

Several statements from Alameda’s executives themselves bolster this theory. For example, Trabucco describes a news-based trading strategy in April of 2021:

To be clear, he is literally describing taking on leveraged crypto market beta because of an emergent narrative about institutional adoptionーexactly the same reason why many retail traders invested in cryptocurrency throughout 2021.

He also describes longing DOGE over a timescale of multiple months because Elon Musk tweets about it a lot:

Again, let me be clear: this is the exact same sort of talk that you hear from your Uber or Lyft driver, especially close to the local tops of the bull market, about the $50 that they put into DOGE and SHIB turning into $200. This is not a sophisticated algorithmic trading strategy by any stretch of the imagination.

There’s no doubt that their BTC and DOGE longs, as described, made money. And there’s perhaps even an argument to be made that they were reasonably smart trades! The more important point, perhaps, is that this is simply just not “quant trading” and that Alameda is clearly expanding into territory where their edge, relative to other market participants, is much less quantifiable and seems relatively disconnected from their areas of expertise. They may have won on the trades they showcasedーbut what about trades where they didn’t win?

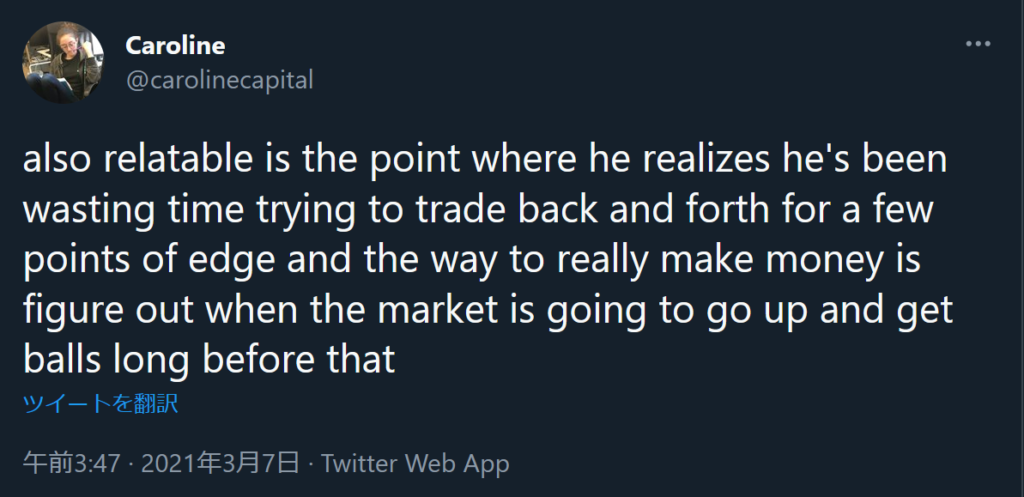

Turning to Caroline, she herself, a month ago, strongly implies that she prefers to punt on longs rather than pick up pennies in the algorithmic jungle:

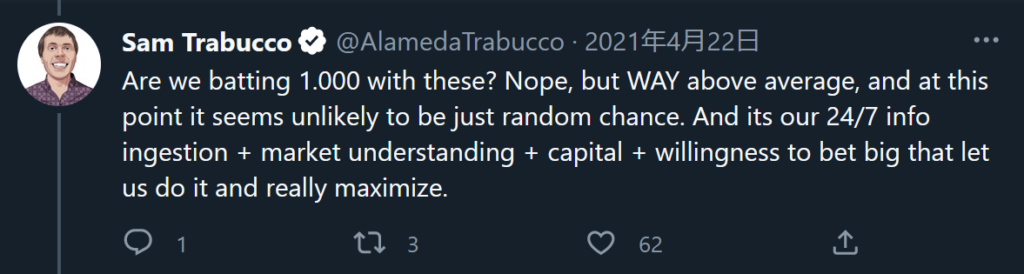

Naturally, these strategies do very well in a bull market, when almost every long position goes up! Remarkably, Trabucco attributes their success to skill rather than simple market beta:

We can therefore speculate that their trading strategies were a combination of (1) negative-edge market making and (2) discretionary longs. Indeed, the more unprofitable their algorithmic trading was, the more tempted one imagines they were to make back all the losses with “brilliant” longs on BTC and DOGE. On net, it is likely that they were quite profitable throughout a good deal of 2020-2021, but as soon as the market began to reverse in late 2021, it is probable that their overall PnL suffered dramatically.

There is definitely a lot of discretionary trading that Alameda did do correctly; buying Solana at low prices, accumulating massive quantities of low-float Solana ecosystem tokens, boosting the Solana ecosystem overall, buying oversold liquidations, and so on. Ultimately, though, one gets the sense that perhaps they overextrapolated from the ambient bull market and ended up overrating their own trading ability, with consequent losses later down the line. Their strategy of borrowing against illiquid ecosystem coins (discussed in a later section), rather than selling them more consistently, may also have worked to their detriment.

We can make one final speculative observation about Alameda’s trading expertise. It is typically very common for alumni of the top trading firmsーJane Street, Optiver, Tower, SIG, and so onーto go on to start their own proprietary trading groups using the wisdom and expertise they have developed. For example, Wintermute, a very successful DeFi-focused market maker, was started by Evgeny Gaevoy, who previously worked at Optiver. Alameda, too, was started by SBF, an alumnus of Jane Street, and eventually co-led by Caroline and Trabucco, from Jane Street and SIG respectively. It is therefore curious, then, that we know of no notable trading firms founded by Alameda alumni, or even of individual traders from Alameda known for their skill in algorithmic trading. The only known Alameda spin-off, so to speak, is a relatively obscure firm founded by employees who left over ethical disputes (discussed further in Postscript #2). This suggests that Alameda itself was not exactly a treasure trove of cutting-edge quantitative expertise.

To the astute reader, one part of the above narrative may seem rather odd. Suppose that you look at your internal PnL graph and you see that your market making is in the red every single day; wouldn’t you simply… turn off your quoter? Well, not necessarily. It is easy to imagine that they justified the market making in terms of the inflated trading volumes it generated on FTX, which in turn justified higher venture valuations for the exchange. Beyond that…

Alameda was an incredibly disorganized, poorly run trading firm

Working at the top trading firms for a couple years clearly does not mean you are a top trader. It also does not mean that you are good at organizing business practices.

An ex-Alameda employee on the Effective Altruism forum shared this telling account of Alameda’s internal practices:

This comment is merely an anecdotal account based on the commenter’s personal memories; however, certain of the details mentioned are corroborated by personal accounts that have been communicated to me privately, which makes me inclined to believe that this is a legitimate and largely accurate portrayal of Alameda’s internal operations. It describes a truly sorry state of affairs, with incredible amounts of money lost to poor bookkeeping, arbitrary discretionary trades under SBF’s direction, internal mismanagement, and incredibly poor organization.

Again, this picture is consistent with a number of stories I have heard via trusted sources, both firsthand and secondhand, all painting a picture of extreme organizational dysfunction, fragmented information, and poor capital management. For example, a personal friend whose company received venture funding from FTX remarked that despite falling very behind on a prior commitment to providing monthly status updates, nobody from Alameda ever bothered to follow up with them. Other accounts are quite similar, and all describe a company culture best described as “flying by the seat of one’s pants.”

If a firm is incapable of scaling back a $3m/year AWS bill or even tracking whether or not millions of dollars’ worth of payments have arrived or not, what are the chances they have accurate tracking of their PnL, let alone a clear view of the state of their assets and liabilities at any given moment? I would say those chances are quite poor. Even if they saw their market making strategies lose money every day, it is not difficult to imagine them saying to themselves: “Well, we may be down a hundred thousand dollars today, but our locked tokens or long positions have appreciated millions of dollars’ worth of value; even applying a large haircut to be conservative, we are still ahead. Why turn off the quoter and jeopardize liquidity at FTX? Instead, we can just throw an intern at the algos and see if they can fix them. If not, no huge loss.”

When you only have a vague understanding of your company’s books, especially considering the incredible amounts of money that FTX expended on advertisements, branding deals, and other discretionary expenses, it is likely that they did not realize the severity of their situation until their loans started being recalled after the LUNA implosion. When you actually have to come up with money and find yourself short, it is at that point which you have to confront your enormous losses, and likely tempted SBF et al. to shore up what they hoped was a temporary deficit with customers’ deposits from FTX. That, in turn, prompted yet more degenerate, riskier forms of gambling, digging the hole even deeper…

Sam Bankman-Fried was erratic, rash, and potentially incompetent

At the end of the day, though, isn’t it weird for a group of ex-traders to engage in such reckless behavior? Although we know little about Caroline and Trabucco personally, we thankfully have a surplus of anecdotes about SBF as an employer and manager.

It is important to note that we should take any personal anecdotes quoted below with a grain of salt. It is always easy to come out after the fact and say that someone who was accused of a crime clearly showed signs of criminality before the fact. Nevertheless, they are consistent in the behavior they describe as well as consistent with non-anecdotal observations made below.

It’s clear that SBF had an “enormous appetite for risk,” as an ex-FTX employee commented:

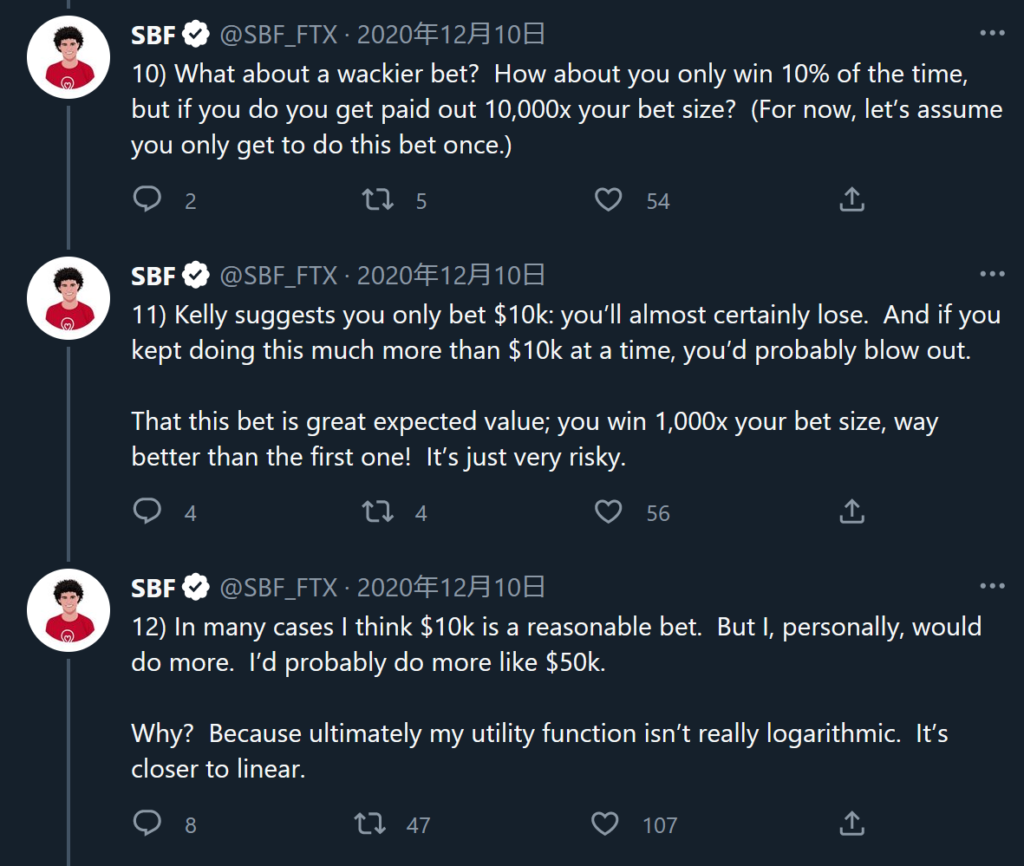

In fact, SBF is on the record as denying the applicability of the Kelly criterion for bet sizing:

To be entirely clear, this simply does not make sense in the case of repeated bets. As Matt Hollerbach points out, this misunderstanding arises from conflation of the arithmetic and geometric growth rates of wealth over time. SBF is provably wrong about this, yet refuses to reconsider his logicーa curious quality for someone who worked at Jane Street and studied physics at MIT!

Why might SBF be so insistent on intentionally oversizing his bets? Purely because of intellectual confusion about what strategy is optimal for long-run growth? An alternative hypothesis is that, beyond any natural proclivity to risk-taking, he may have been taking dopaminergic drugs (prescribed for for Parkinson’s disease) as a nootropic. These drugs as well known to cause risky behavior such as compulsive gambling or shopping sprees!

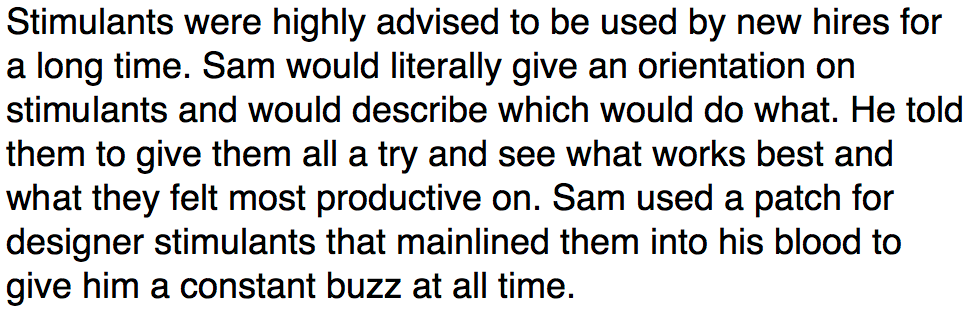

Autism Capital recently shared an account from an ex-FTX employee recounting how SBF encouraged extreme use of stimulants:

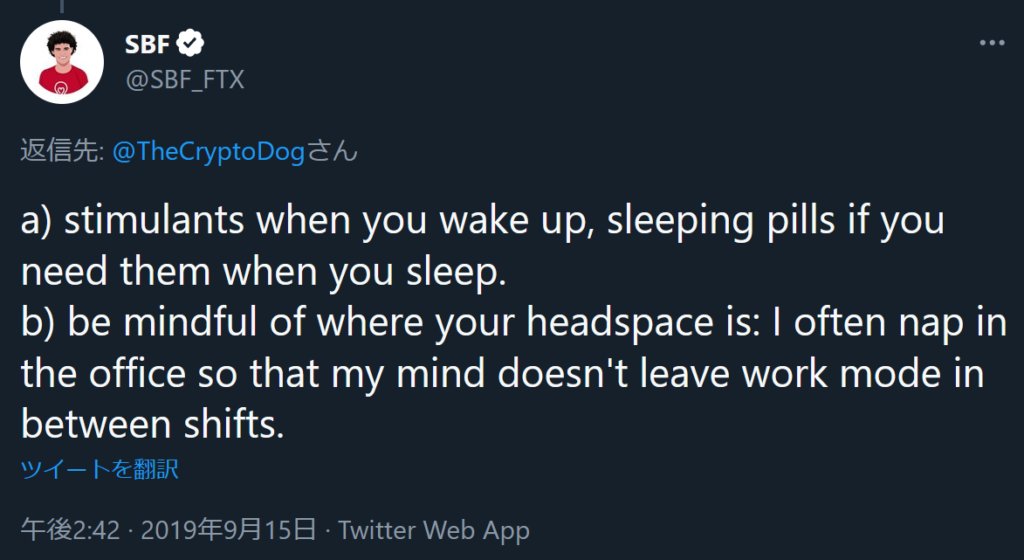

This is, of course, consistent with SBF’s self-admitted usage of stimulants as performance enhancers:

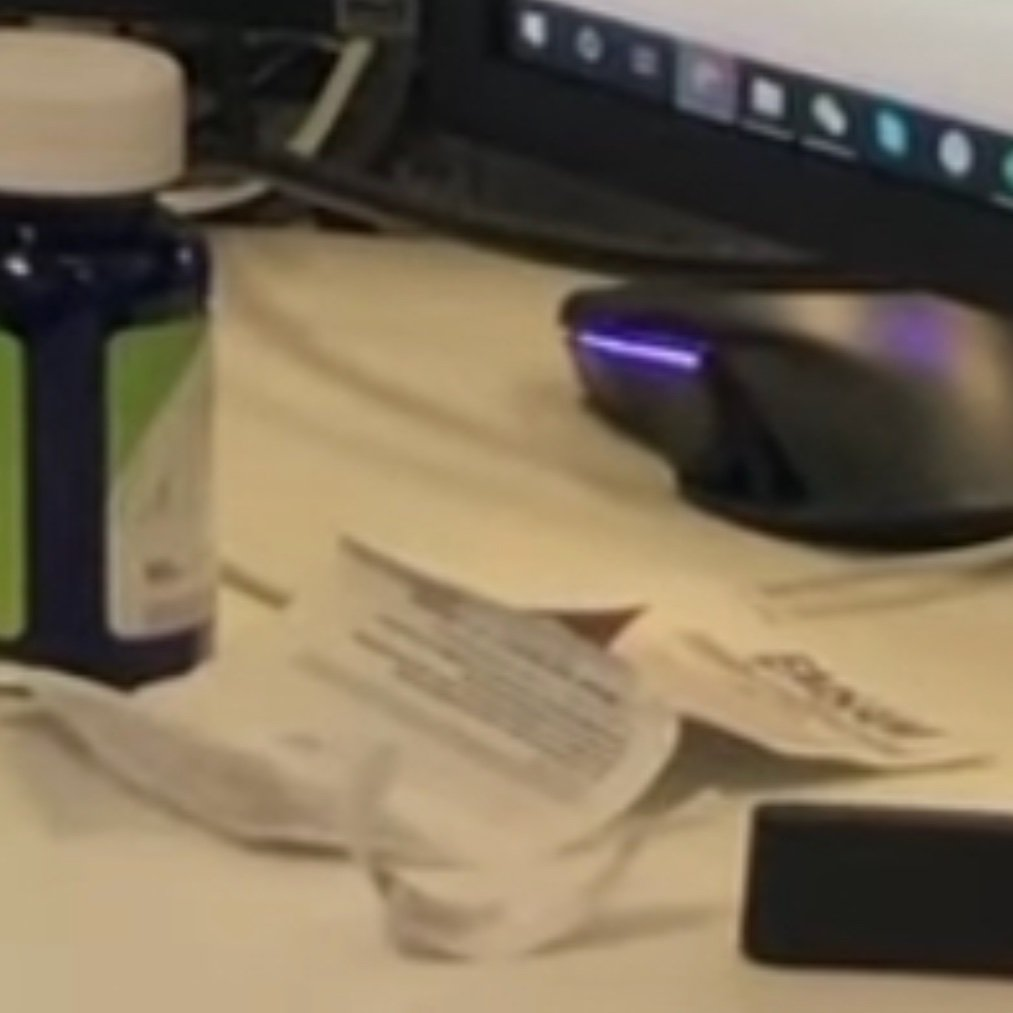

What is particularly notable, however, is SBF’s usage of “patch[es] for … stimulants.” In a follow-up Tweet, Autism Capital reports that the patches are Emsam (US brand name for selegiline), a MAO-B inhibitor used to treat Parkinson’s which increases levels of dopamine in the brain. This was confirmed with some excellent follow-up detective work, also from Autism Capital, which pinpointed a particular video frame from a video showing SBF at his desk:

If you zoom in, you can see what appears to be wrappers for some form of medication:

These match perfectly with Emsam’s commercial packaging!

Dopaminergic medications for Parkinson’s disease have long been associated with extreme risk-taking, such as in this study of pathological gambling in PD patients taking medication:

Many other such references exist in the literature. Remarkably, there is even a case study of selegiline-induced hypomania, as well one reporting hypersexuality and paraphilia! Overall, it seems very likely that SBF’s propensity to take extreme levels of risk was elevated to preternaturally high levels via heavy, habitual usage of amphetamines and selegiline, causing him to rationalize nonsensical strategies as optimal via convoluted “linear wealth utility” reasoning.

Note that PD medications have also been strongly associated with the development of compulsive shopping. FTX’s massive spending on advertisements and branding partnerships may very well have been a ploy to attract deposits, but it may also have been driven, in part, by SBF’s continual abuse of these drugs. For example, there are reports that a $12 million ad campaign with famous Japanese baseball Shohei Ohtani was killed after a single day on air. Similarly, FTX acquired naming rights to the e-sports organization TSM for a stunning $210 millionーfar out of line with comparable deals in the e-sports industry. Even his property acquisitions are stunning, with a reportedly $200m real estate portfolio in the Bahamas. These cannot be rationalized as risky bets with positive expected value, and only make sense in the context of executive management which is either incompetent or, as we suggest, literally drugged up and on a multi-year shopping spree.

One can also argue that there are clear signs of SBF’s deficits in the realm of overall competence and cognitive ability. For example, his personal blog, Measuring Shadows, is incredibly dullーit is a compendium of overly long posts about effective altruism, moral philosophy, and baseball statistics. In comparison, Caroline Ellison’s blog is far superior, demonstrating a level of thoughtfulness and wit that surpasses SBF by many leagues. Perhaps more tellingly, the Financial Times reported that SBF is remarkably bad at League of Legends:

While this may initially seem like a frivolous observation, it is actually shocking that SBF was unable to rank higher than the Bronze or Silver league after years of regular play across hundreds if not thousands of individual games. It is reflective of an incredibly impaired level of cognition, much like someone who was unable to learn how to ride a bicycle after an entire month of practice or someone who never progresses past the level of an average elementary school student after five years’ of daily piano practice. To me, this is one of the strongest indications possible that SBF is, to be blunt, “not entirely there.”

Just in the last 24 hours, SBF has been tweeting out the phrase “What HAPPENED” letter-by-letter, with gaps of hours between some tweets:

This is, frankly, just absurd and incomprehensible. It makes absolutely no senseーwhat is he doing? What could be possibly hope to accomplish with this? I struggle to imagine the state of his mind at the moment. Does he think that this is an elaborate joke? Is he hopped up on a metric ton of obscure drugs and beginning to lose his sanity? Neither of those bode well for the integrity of his cognition. (It was originally speculated that this was some bizarre scheme to avoid having deleted tweets show up on deletion trackers, but that theory has since come under criticism.)

How do we reconcile these observations with SBF’s MIT degree, Jane Street pedigree, successful execution of international Bitcoin price arbitrage, and the founding of Alameda Research and FTX (which, even if ultimately failures, still required some degree of executive function to actually start)? It is not clear, but one could speculate that excessive drug usage may have literally “fried his brain” to some extent. Ultimately, it is challenging to speculate about why his cognitive performance has degraded to such a poor level, but the fact remains that it does appear to be quite poor.

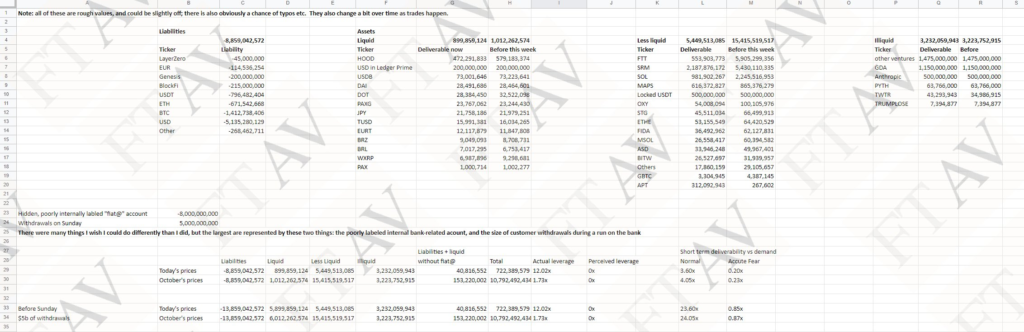

One cannot help but wonder if this general deficit in intellectual ability is why the FTX balance sheet (provided by SBF earlier last week) is so farcically simplistic:

Frankly, this can barely be considered a serious attempt at accounting. It is so absurd that one’s initial assumption is that it is some sort of insane attempt at the financial equivalent of “making up an answer when the teacher calls on you.” But what if this is actually reflective of the quality of his thought.

If the above observations about SBF’s personality and competence are even half true, that would go a great deal toward explaining Alameda’s losses. (Even though he formally stepped down as CEO, he of course maintained a close relationship with Caroline and Trabucco.) In particular, once customer deposits were raided, he may very well have tried to “make it all back” in increasingly desperate attempts that just dug the hole deeper and deeperーhardly unsurprising if he indeed was actually operating as a mildly brain-addled compulsive gambler.

Collusion between Alameda and FTX caused huge losses from algo failures

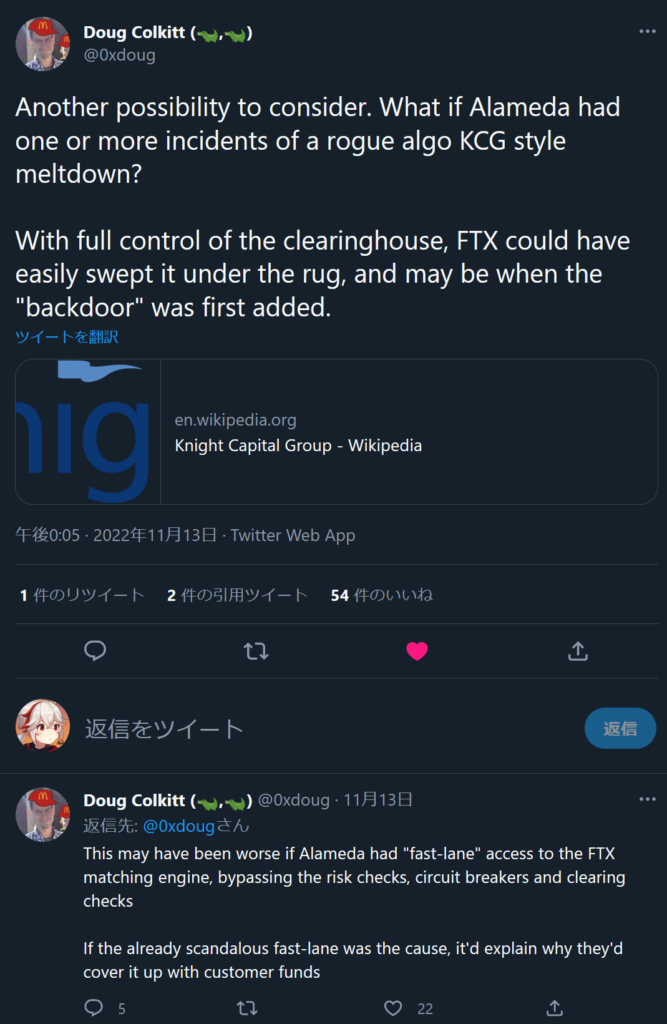

It has long been suspected, and corroborated by multiple reports, that FTX and Alameda were essentially operating in total collusion, with Alameda frontrunning token listings and potentially having special privileges to bypass risk checks. (The famously slow latency experienced by API traders on FTX may have been essentially engineered as an artificial barrier that only Alameda could skip.)

Doug Colkitt speculated that this could actually have caused an “algo meltdown,” similar to a well-known incident with Knight Capital Group in traditional markets:

Reports communicated privately suggest that this may have actually been the case, resulting in losses potentially in excess of $1 billion dollars! And, of course, there may have been other incidents not known to me.

Without full access to FTX’s records, it is challenging to really confirm or deny these claims, although the sources are credible, and I am inclined to believe them. If true, the scale of these losses is more than enough to be a major contributor to FTX & Alameda’s overall shortfall.

Loans collateralized by FTT/SRM resulted in reflexive liquidations

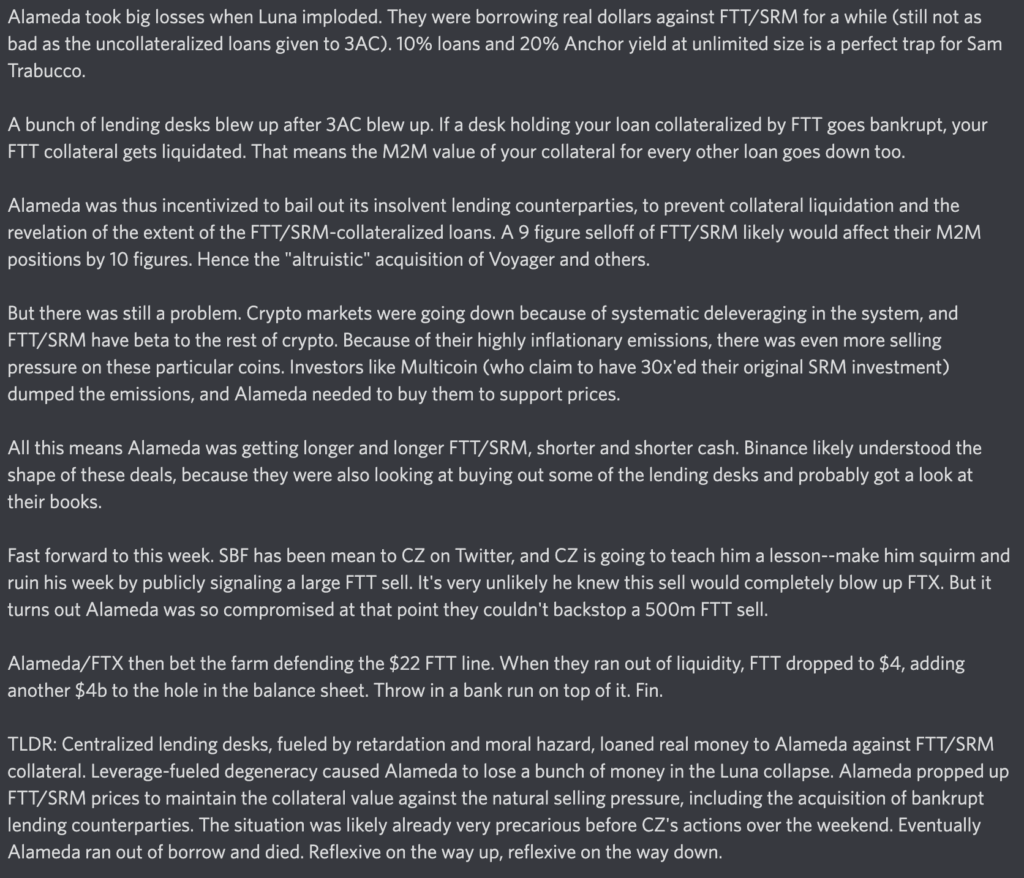

A trusted friend (non-insider) anonymously shared the following theory with Autism Capital, which I will reproduce here in full as it is clearly and concisely written:

The theory is quite convincing, and boils down to an increasingly desperate series of attempts to backstop a series of reflexive liquidations of loans backed with illiquid shitcoins (FTT/SRM). Because of token emissions, even maintaining their prices at a constant level requires a constant inflow of capital, continually increasing Alameda’s exposure to these coins and reducing their cash reserves. Ultimately, they ended up in a vulnerable position where they simply ran out of the money required to meet demand for customer withdrawals while preventing a collateral liquidation cascade.

In isolation, I am not sure if this theory fully explains the losses suffered by FTX and Alameda. However, positioned in the context of the other theories advanced above, it is certainly plausible that this theory explains a fair portion of the shortfall.

This theory dovetails well with Caroline’s admission that FTX transferred over customers’ deposits after the LUNA crash in order to repay recalled loans. In particular, it provides a reason as to why FTX was essentially compelled to bail out insolvent lenders like Voyager and BlockFi. On top of loans recalled by other entities, such as Genesis, this would represent a substantial and unanticipated short-term demand for cash. If Alameda was already operating with poor bookkeeping, and especially if Alameda were substantially exposed to the LUNA crash itself, it becomes increasingly easy to imagine that SBF et al. felt they had no other option than to dip into customers’ deposits.

Summary

So, what have we really learned? In the end, we don’t actually have a great idea of exactly how Alameda and FTX burned through as many billions of dollars as they did. However, there are sufficiently many competing theories available, each with a sufficient amount of supporting evidence, that I suspect that the reality of the matter looks something much like a combination of all of the above factors.

We can try to give a very rough accounting of their potential losses:

- Voyager/BlockFi acquisition: 1.5b

- LUNA exposure: 1b

- KCG-style algo crash: 1b

- FTT/SRM collateral maintenance: 2b

- Venture capital: 2b

- Real estate, branding, other frivolous spending: 2b

- FTT drop from $22 to $4: 4b

- Discretionary longs going bad: 2b

- Total: 15.5 billion

This is, of course, very rough. I have no idea how much they lost in LUNA or how much they might have blown on longing shitcoins. I have not bothered to actually calculate out the total of their venture investments, nor have I gone and added up every single one of their branding partnerships. Yet the overall picture is clearーwe have enough potential sources of losses that even if some of the numbers are off here and there, it is now at least conceivable how they might have arrived at such staggering losses. You can make up your own numbers, but the point is that there are many reasonable combinations of figures above that could result in losses equaling or even vastly exceeding $15 billion.

I make no claim to the ultimate veracity of the above information. Instead, my purpose is largely to compile these here into something of a patchwork narrative, which I do not believe exists at present. The reader is invited to draw their own conclusions!

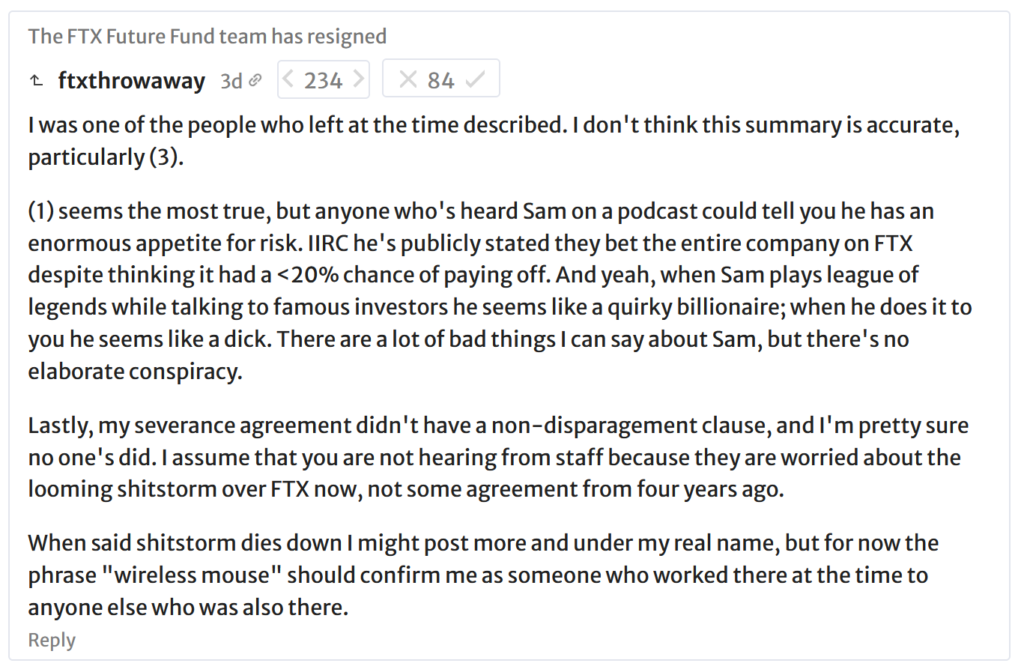

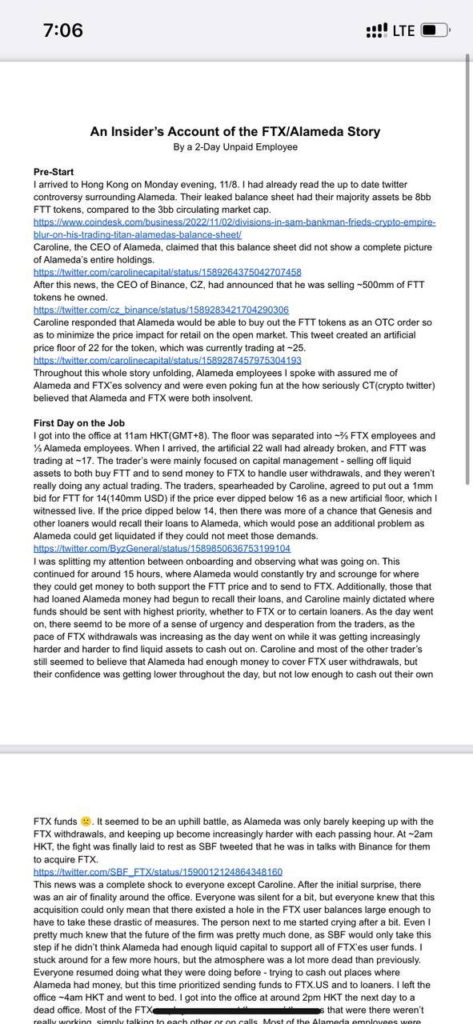

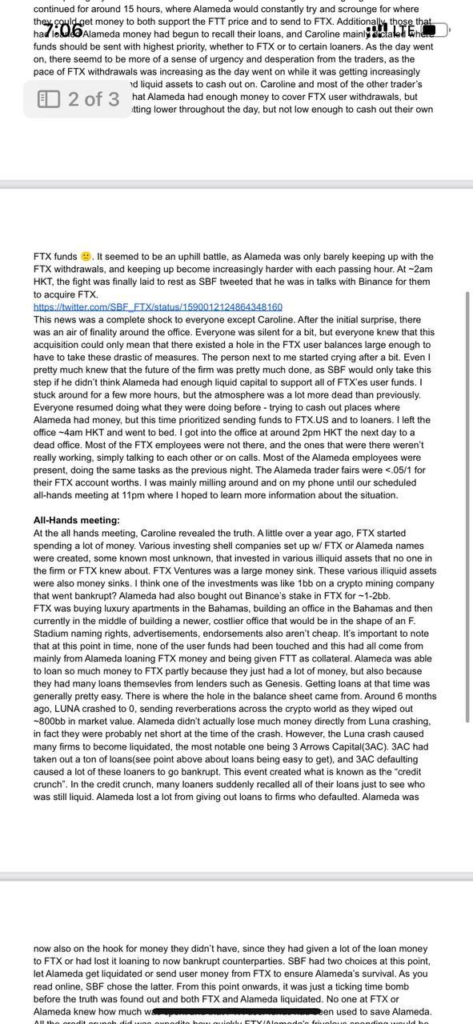

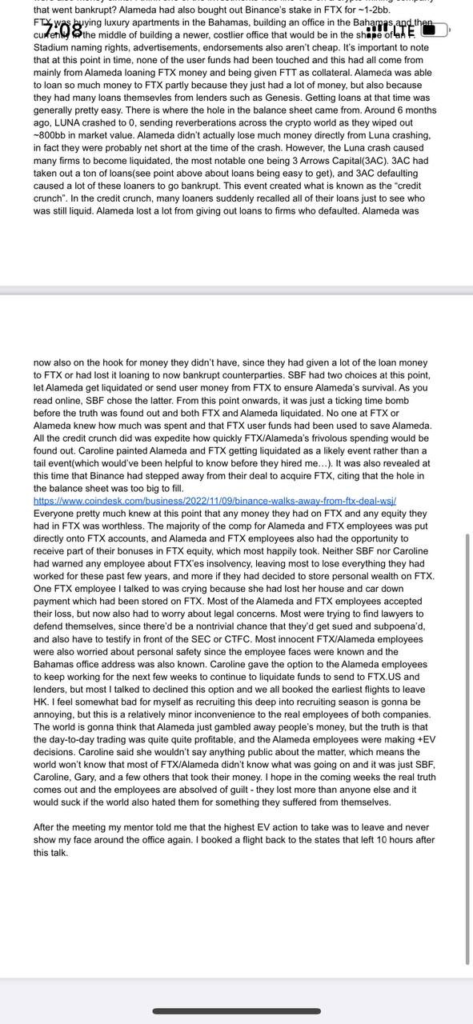

Postscript #1: An insider’s account of Alameda’s final days

@libevm posted screenshots of an anonymous Alameda employee’s account of their first and only two days at Alameda Trading, which I reproduce below for the sake of posterity:

This sounds like an accurate rendition of Alameda’s final days to me, and is consistent with other scraps of information that I have heard. From this, we can add a couple more estimated expenditures to the final tally:

- Buying out Binance’s stake in FTX: 2b

- Loans to companies which defaulted from the LUNA collapse: 1b

I am a little skeptical of certain claims. For example, if the employee only worked there for two days, they likely did not really know for themselves that the trading was +EV, although they could have chatted with their coworkers, I suppose. Also, even though FTX clearly spent money freely and frivolously, the degree of known spending is simply not enough to account for the missing money in their balance sheet! Nevertheless, as far as the author’s lived experience is concerned, it reads as a faithful account.

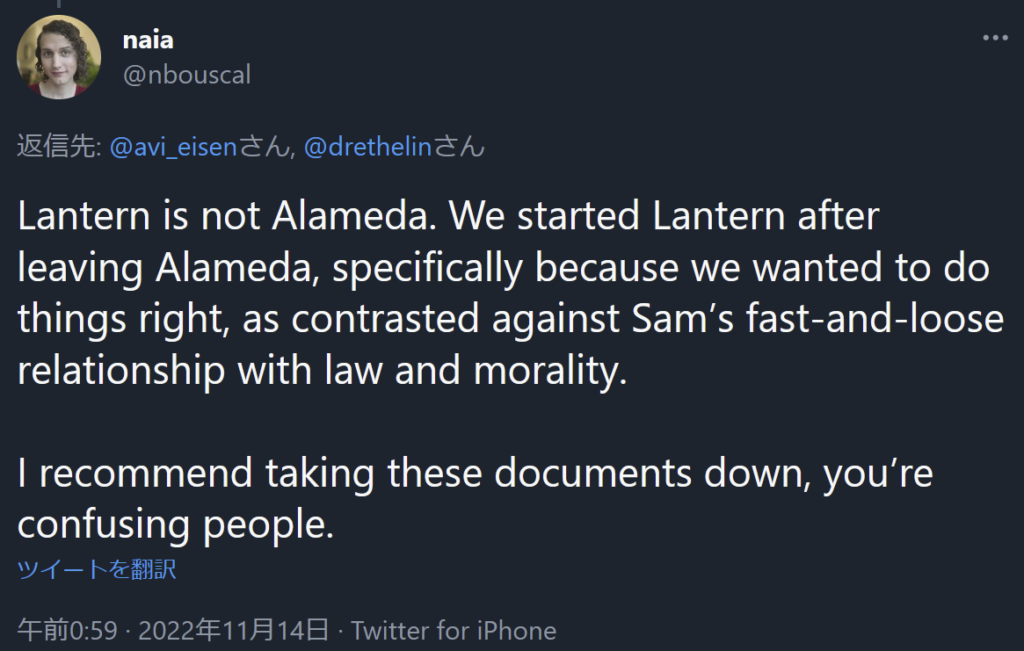

Postscript #2: Lantern Ventures and Pharos Fund

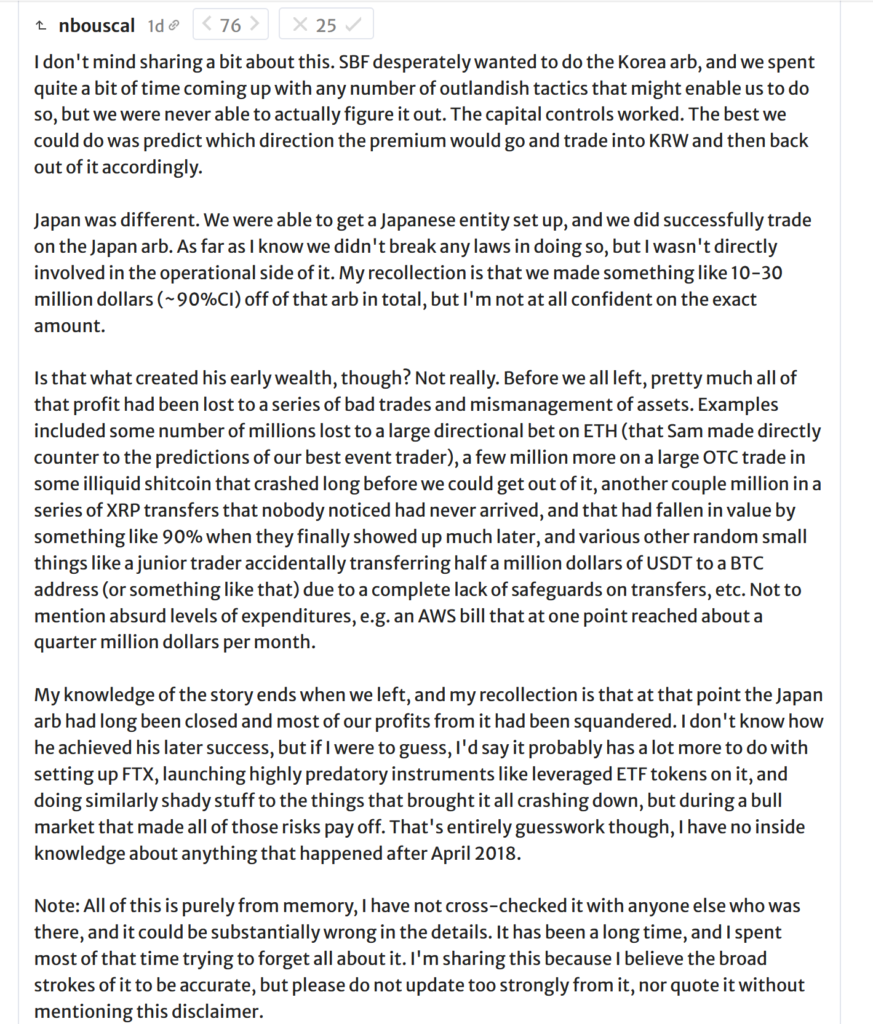

As discussed earlier in the article, we do not know of any notable trading firms founded by Alameda alumni, suggesting that Alameda itself was not in fact especially skillful in quantitative trading. However, we do know that a group of employees, including a co-founder of Alameda Research (Tara Mac Aulay), left Alameda Research in 2018 over ethical concerns. In Tara’s words:

Another ex-Alameda employee who joined Lantern, Naia Bouscal, also remarked that they disagreed with SBF’s “fast-and-loose relationship with law and morality”:

To the best of my knowledge, neither Lantern Ventures nor Pharos Fund are particularly well-known. Indeed, almost no quantitative trader I know has ever heard of either one until now.

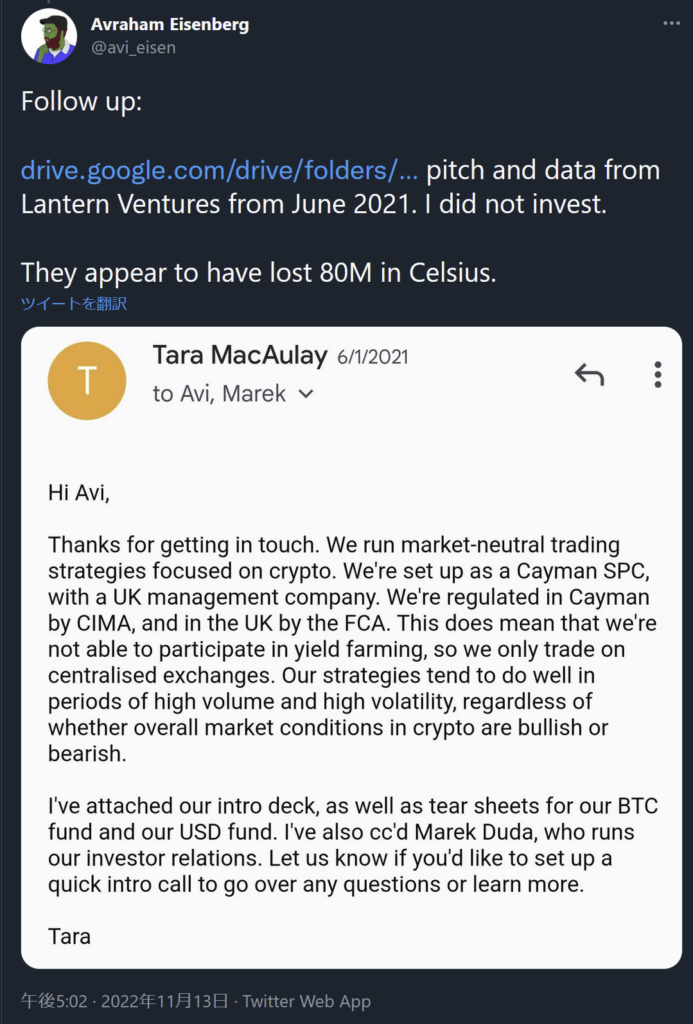

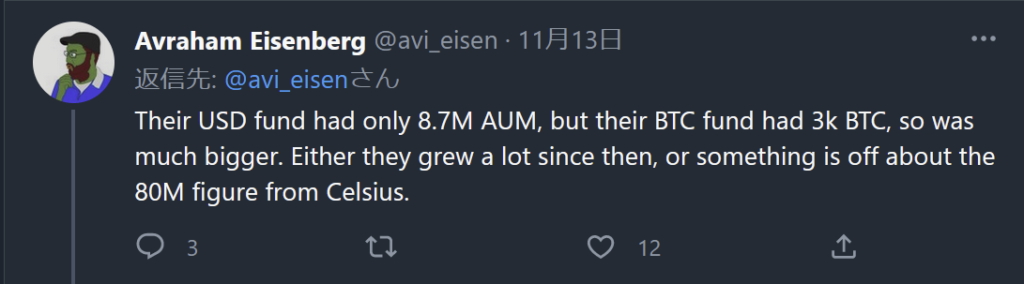

It is difficult to objectively evaluate their competence without knowledge of their fund’s performance and operations. However, one telling indication comes from Avraham Eisenberg, who cited LP pitch materials sent to him by Lantern in June 2021 and indicated that they lost 80 million dollars to the bankruptcy of Celsius Network:

How large are these losses in proportion to their overall AUM? Avraham also supplies some figures:

Estimating the price of Bitcoin as $35,000 (approximately the closing price in June 2021), it appears that Lantern Ventures’ AUM was approximately $115 million.

Even more curiously, a Substack post (PDF) by Dirty Bubble Media made some fascinating observations about Pharos Fund’s inclusion in the Celsius bankruptcy documents. For example, the contact information given for Pharos is a Lantern Ventures e-mail address, suggesting that the two entities are closely related. More interestingly, the author also notes that Lantern’s balance sheets indicate they were worth as little as £3.1 million in May 2021. Yet at the same time, the author comments:

According to Bloomberg, SEC filings indicated Lantern was managing a total of around $400 million in April of 2022. The question remains: Whose money were they “managing?”

Either way, what is clear is that Lantern & Pharos seem to have lost a significant percentage of their AUMーat least 20%ーto the bankruptcy of Celsius Network, a centralized cryptocurrency lending platform which was known as far back as in 2020-2021 to be delivering suspiciously unsustainable yields to depositors (and, therefore, was likely to be a Ponzi scheme doomed to eventual collapse). This, combined with the lack of industry recognition, suggests that they were themselves not particularly sophisticated operators, further cementing the conclusion that Alameda itself did not possess exceptional skill in trading cryptocurrency markets.

November 15th, 2022 at 7:24 am

Sam does prescription stimulants and writes a midwit blog and loses his mind. Caroline endorses prescription stimulants on her brilliantly written blog, but is also probably partially complicit in torching billions of dollars, albeit with a bit more apparent lucidity.

are the stims based or not???

November 15th, 2022 at 7:26 am

Effect is mediated through intrinsic basedness of the user

November 15th, 2022 at 9:44 am

That’s some serious investigative journalism, good job.

November 15th, 2022 at 9:55 am

Absolutely outstnading and insightful. Thank you.

November 15th, 2022 at 10:14 am

BS. this and other articles are just cover for SBF/Caroline. they are criminals that have zero sympathy for you. this is just a charade to put the blame in incompetence rather than maliciousness

November 15th, 2022 at 10:53 am

I was here

November 15th, 2022 at 11:22 am

Everything is summarize on my name

November 15th, 2022 at 12:26 pm

Anyone on powerful enough to take on governments? Dms open. Google docs hangouts cool too x

November 15th, 2022 at 2:58 pm

Thanks for the journalism. This does seem to exonerate Caroline’s father thougg. I do think all the conspiracies are a bit out there, but the Caroline’s ascent from trader to co-CEO to CEO seems to be because of her father and his connections. After all, CEOs are just a face of a company designed to raise money and steer the metaphorical ship. They network, make bold decisions and cash out. Hope she still has good ones in HK…

November 15th, 2022 at 3:11 pm

damn, you really gonna make me direct my parents to read a post on milykyeggs.com written by 0xfbifemboy…………

the simulation intensifies

November 15th, 2022 at 3:14 pm

And if you ask me, it’s just a big laundromat to move money from the Ukraine into other’s pockets.

November 15th, 2022 at 3:43 pm

Something is off with the 2 day story. The facts are plausible but the style and the way it is put together feels like a lie. Maybe it’s a longer term insider trying to pretend otherwise (could be Caroline herself) or pure fan fiction based on publicly known facts (it does not reveal anything probably original).

November 15th, 2022 at 4:52 pm

Great work.

November 15th, 2022 at 6:21 pm

What is the best explanation for why it took so long for all this to come out? As you point out, there are hundreds of highly-motivated people who knew all this stuff (specifically the key feature of “we don’t have billions of dollars we said we did”) months/years ago. Surely there was some way for us to have read this 6 months ago.

November 15th, 2022 at 6:27 pm

I wish I could buy equity in this site lmao

so fking good

November 15th, 2022 at 7:17 pm

[…] 6. What exactly happened at FTX? […]

November 15th, 2022 at 7:49 pm

You ask why the tweets this morning: what happened.

This looks like part of building a criminal defense. You see SBF saying various things like poor controls, he was distracted and had other priorities, he was duped by some unscrupulous or stupid underlings, etc. This is all aimed at showing lack of knowledge and intent. (Note that he may actually lean into the drug portion of the story also.)

He is going to face criminal wire fraud charges. He knows it. He’s consulting with a criminal defense attorney. This is exactly what any defense attorney would tell him to do.

November 15th, 2022 at 7:55 pm

Shitcoin Icarus gets wasted trying to be boy wonder. This reads like if the Wolf of Wall Street had a retarded brother in crypto.

November 15th, 2022 at 8:04 pm

I would say the article is at its best when it’s evaluating the financial aspects and at it’s worst when it’s evaluating the role of drugs, etc…

It’s pretty clear that FTX and Almeida were riding a bubble being driven by VCs eager to get in on what looked to them like a growth industry with retail “investors” hoping to make a killing on a new and exciting lottery ticket.

They needed to keep making deals, however insane, in order to justify their valuation to the VCs that were infusing them with cash. Otherwise, they were just another late stage startup looking to be bought, at an almost reasonable price, by an established player looking to get in on the crypto market.

Add to this that they had all the regular leitmotivs of fraud: domineering CEO, inexperienced managers, complex financial instruments, self-dealing, and no effective compliance or audit function.

No different than Enron, Bear Sterns, Allianz, etc…

As to the rest, many have played League of Legends for years are barely ranked above Silver and many people, even smart people, write boring blogs.

November 15th, 2022 at 8:22 pm

Being hard-stuck Bronze 3 as a measure of the cognitive ability of a billionaire entrepreneur was not on my bingo card for 2022. Jokes aside, the majority of players play with their brains off and just play League out of an addictive need to have it on in the background and to kill time rather than as an opportunity to improve at the game. Rather than a proxy for cognitive ability, I would use being hardstuck as a proxy for a non-competitive / non-initiative-taking personality. That may or may not be a result of drug use.

November 15th, 2022 at 9:35 pm

This post has a lot of good reporting and analysis, but I take issue with the extent that you read into certain aspects of the SBF story.

1) on LoL: it’s certainly odd that SBF never made it higher, but cognitive impairment isn’t the only explanation. We know he played it during meetings sometimes — if his attention was split much of the time he was gaming, that could account for underperformance, and doesn’t seem at all implausible to me.

2) on his blog: I don’t think this really counts for much of anything at all, and I think including it at all sort of weakens your post a bit.

It doesn’t appear to have been updated *at all* since 2016, and the bulk of the posts are from 2012 — *ten years ago.* Are you trying to suggest that his brain has been “fried” for the last decade? (SBF, now 30, was 20 and still in college in 2012.) Moreover the fact that it’s not terribly engaging to read isn’t surprising. Plenty of smart, functional people maintain blogs that aren’t particularly colorfully written, for various reasons.

Caroline’s blog on the other hand was part of the rationalist tumblr social community. She used it to make jokes with her friends, share thoughts on her personal life with them, etc. It was part of her life in a way that Sam’s blog clearly wasn’t. The two blogs seemed to have very different goals and existed in wildly different contexts. It’s an extremely tenuous comparison imo, enough that I felt compelled to write this comment.

Overall I agree that his behavior was highly erratic and disconcerting in general, and that *may* be reflective of general cognitive impairment, but you don’t really acknowledge other possible explanations for the behaviors you pick out, and it kind of weakens your post, which is a shame since it has a lot of good in it.

November 15th, 2022 at 10:04 pm

I think that since FTX invented FTT, it declining in value loses part (eventually all when it zeroes) of their previous gains, but FTT declining in value does not account for any lost customer funds. Spending money defending the value of FTT absolutely does account for some of the lost customer funds, though. Also, spending money on perks for FTT holders costs FTX money, but that amount is likely small and overwhelmed by the monthly millions FTX made in trading fees.

November 15th, 2022 at 10:38 pm

Am I the first to notice how incredibly lazy it was to cite a value of $2,187,876,172 for the SRM tokens?

Just look at how lazy it is to make that number up. Put your left hand fingers on the “1” and “2” on your keyboard. Put your right on “6” “7” and “8”.

What sounds good? A 10-digit number? Okay, smash out a ten digit number.

In my day we used made up numbers from all over the keyboard, not this lazy stuff. Freaking kids.

November 16th, 2022 at 12:33 am

Who is Gary Wang?

November 16th, 2022 at 12:43 am

Yet if they were a traditional Wall Street investment bank they would militantly demand to be “recapitalized” by the Fed and the Fed would do it too. Not one executive would be facing criminal charges, heck, they would even receive their year end bonuses.

As bad as SBF & co are, they are not any worse than the Goldman Sachs and the Citibanks and the Bank of Americas who got bailed out without questions by the Fed and Congress and Obama. And took home their “bonuses” too.

November 16th, 2022 at 3:30 am

I’m not an insider at FTX, but the 2 days story reeks of fanfiction. I have worked in the trading industry and everything makes no sense, this isn’t how any of this works. They said the first day “continued for 15 hours” like working a 15 hour shift on their first day is normal. How the heck do you get this much detail from your first day working somewhere:

“As the day went on, there seemed to be more of a sense of urgency and desperation from the traders, as the pace of FTX withdrawals was increasing as the day went on while it was getting increasingly harder and harder to find liquid assets to cash out on.”

On your first day you wouldn’t even understand what most of the other employees are talking about, let alone know that the pace of withdrawals was increasing, the difficulty of “finding liquid assets to cash out on”. It also would be every single one of the “traders”’ lowest priority in such a situation to make sure a new person knows about any of this.

And who in their right mind schedules an “all-hands meeting” at 11pm? I get this is supposed to be a crisis but there’s still no way you have everyone there at such a random time.

This is just my qualms with the very beginning of the story. I would highly recommend you remove this work of fiction unless it’s corroborated with actual meaningful evidence. It damages the credibility of the rest of your information and adds no substance.

November 16th, 2022 at 3:34 am

I mean if your point is like “this makes no sense, this seems nothing like how a regular trading firm was run,” that seems par for the course? I trust the source

November 16th, 2022 at 7:32 am

Best piece I have read on the topic so far. Thank you for putting the time into this – I bet it took a lot of work.

Was fully invested until the very last statement of the “2 day employee”. No fault of your own, btw.

“After meeting with my mentor, he said the highest EV action was…”

Anyone talking like that is an Opp. EV action? Cmon. Reeks of failed consultant/top firm trader position. Makes me retch.

November 16th, 2022 at 7:33 am

@Anon — you say “On your first day you wouldn’t even understand what most of the other employees are talking about” — are you sure you wouldn’t be able to figure it out over the course of 15 hours though? Just by talking to people who were taking a break or whatever?

November 16th, 2022 at 11:49 am

Best single piece of recap out there. Fab work.

Agree with your assessment of their severe alpha decay and increased punting. The other downfall is that out of the entire leadership of Alameda/FTX, no one is trained to understand the changing macro backdrop and fundamental regime shift this past one year. Cathie Wood is another macro illiterate out there that bears resemblance – I digress.

Just one assumption I might challenge. While it’s an open secret that exchange make a sh!t ton of money from liquidiations, I actually think FTX may not have stop hunted and capitalized on this source of income as much of some of the OG exchanges (think back to the days of OKex and Bitmex).

I had tasked one of our junior traders to test out liquidations on FTX, it turned out 1) blanket margin confiscation problem was a lot less prevalent on FTX and 2) decremental liquidation was more commonly observed than peers, even for tiny positions. And you juxtapose this with the fact that they were first to enable 7-day TWAP this year, which if you think about it, is completely antithetical to the idea of maximum rekking – since it allows retail traders to avoid liquidations, reduce impulsive trading and ease into leveraged positions etc.

This certianly would imply they took the high road when it comes to liquidation. What’s their motivation though? I’m not sure. Maybe they were too self-aggrandized gawking at the headline MTM of their venture books and success of FTX. But above is of any indication, this could take off a few billion from your estimate of $10b profits generated between alameda and FTX.

November 16th, 2022 at 12:52 pm

One point about League of Legends, Bronze mean SBF is between about the 5th and 25th percentile, Silver means he’s between around 25th to 55th percentile. Most casual players are in those tiers, and experience doesn’t mean much, especially since the game is constantly changing. Getting above Silver requires putting in effort, if you just play a few hours a week for fun you won’t win against serious players no matter how smart you are.

November 16th, 2022 at 1:59 pm

A $3M/yr AWS bill is absolutely fine. If you’re making $100M+/yr on trading, you should put 100% of your employees’ time into increasing top line revenue. Cost cutting can wait until crypto winter.

When retail money is pouring in and people are making billions trading, time is your only real constraint. If you can spend money on capital goods to leverage your human capital, that’s an extremely strong move. Not a sign of incompetence.

Source: personal experience doing exactly this at a large HFT.

November 16th, 2022 at 3:23 pm

Thank you Kanye, very cool

November 16th, 2022 at 3:27 pm

How is this all connected to Nicolai Mashegian, co-creator of DAI, being murdered and dumped in Costa Rica 4 hours after tweeting about a CIA-run pedo op in the Carribean?

How is Sam not in jail?

November 16th, 2022 at 3:52 pm

Why did you delete my question?

I will ask again: How is Sam linked to Nicolai Mashegian, co-creator of DAI? How is Sam linked to Nicolai’s death?

November 16th, 2022 at 4:22 pm

Um, Sam is a puppet. It’s the face of one of the many operations. Vlad was another. Plotkin as an intermediate stooge. The real financial terrorists behind all this are unknown to anyone in the public. Even Ken Griffin is not the highest ranking financial terrorists. It is more of a money man that moves money around and helps enable the stealing.

Just as Nancy “the psychopath” Pelosi got up and lied to the masses about her Homosexual husband’s sexcapade with a male prostitute(and it isn’t his first gangbang), the same is happening with FTX. The true story will never be told and will be actively covered up with lie upon lie so no one knows the truth except the insiders. When the story doesn’t make sense it is because it is a lie. “Some random guy breaks in to our house and tries to murder my dear Paul”… yet no video footage, no actual motive except what they tell us(which is BS because no one does stuff like that. If he went in there to murder him one of them would be dead).

Anyways, same with FTX. No way Scam Bankrun-Fraud pulled all this off himself. It’s simply not possible. Also, all the other scams are the same. In fact, the entire industry is a fraud. It’s all about theft and who can steal the most. Humanity is the loser as the psychopaths engorge themselves on the real working class(the people that do real work to keep everything going… which is why everything is falling apart because they are being raped and pillaged).

There are consequences to letting morons and psychopaths run the show. We’ve just begun to experience the collapse. They’ve destroyed all value. There is no way to escape this black hole. They’ve stolen so much money that no matter what is done they will always have the power to undermine society with their degenerate psychopathic minds.

The masses are to blame. All the useful idiots are more to blame. Everyone was happy when they were getting there thousands in bonuses and got to live in their nice houses and drive their fancy cars to impress their other moronic sociopath friends in one giant jerk fest. Well, the orgasm is coming and all that materialism and ego isn’t going to save any of you and neither is your sugar daddies who actually never gave a fuck about you. Well, they fucked you alright. Welcome to hell. Maybe you will try to strike them with the hammer they shoved up your ass but you’ll still end up buried by them.

November 16th, 2022 at 4:57 pm

[…] Edit Add: This is decent speculation as to the timeline and details of what happened. Unlike the NYT (the “reporter” is obviously bought and paid), this guy knows a thing or two: https://milkyeggs.com/?p=175 […]

November 16th, 2022 at 5:21 pm

That was superb, very detailed and unique view point. I was unaware of the drugs and it really makes sense for them to make him very irrational. Your opening line about the New York Post made me laugh, so true.

November 16th, 2022 at 5:46 pm

Post ID: 659482321842487296

Date: 2021-08-14 08:55:52 GMT

Body: honestly this is so uncool but I love it when fiction has representation of literal girlbosses. like women managing people and running stuff. I’m like omg it me

Tags: #women less likely, #q u a r t e r l y c a p i t a l i s m”

Seriously, this is what passes for a brilliant blog full of thoughtfulness and wit? I guess the bars are lower for social conservatives and women…

November 16th, 2022 at 6:52 pm

> And who in their right mind schedules an “all-hands meeting” at 11pm?

Because that’s 9am in the Eastern time zone.

November 16th, 2022 at 8:55 pm

Seed? Milky Eggs? A whole lot of SDF semen …

November 16th, 2022 at 10:12 pm

So, what’s going on dude, you’ve deleted my posts thrice now.

What’s your angle? You’re letting others here broach a variety of topics, so why not let me bring up the connections between Nicolai Mashegian, co-founder of DAI, and SBF?

What are you trying to hide by not letting this topic be brought up?

November 16th, 2022 at 11:36 pm

@The Noticing: I don’t have time to monitor the comment approval queue 24/7, retard

November 17th, 2022 at 1:19 am

🙂 hehe

November 17th, 2022 at 6:01 am

Not an Investment Bank and Jo Blow win for biggest idiots in the comment section! congrats you fuks! you’re the dumbest with the thickest skulls! your simpleton smooth brains have earned…. shame!

your mothers are disappointed you fall for conspiracies about “The Man”

November 17th, 2022 at 11:51 am

Interesting article – very interested to see how this matches up to the real situation as it unfolds.

November 17th, 2022 at 2:24 pm

[…] Over time Alameda’s market making edge degraded as competitors improved, to the point where they were likely losing money on market making. They get into other things like yield farming and venture, then directional news trading. […]

November 17th, 2022 at 4:55 pm

@People R Dumb

“OY VEY the goyim are noticing!”

November 18th, 2022 at 1:28 am

Oh joy, I arrived just in time for groyper-esque ‘the j00s’ comments.

Hmm, where to begin? Clearly, with praise for Milky Eggs aka clever twit userid @0xFBIfemboy. I will follow you as soon as I finish here. You did a GREAT post-mortem of SBF FTX!!! Also, your grammar and usage is flawless. I appreciated your scholarly journal citations to support your hypothesis about the effects of unrestrained stimulant indulgence on SBF. “Prospective Prevalence of Pathological Gambling and Medication Association in Parkinson’s Disease” demonstrates your attention to detail! Love the alliteration.

SBF might have destroyed his cognitive faculties, but without any adults in the room, there’s no one to tell him to address some of his massive sleep deficit. His risk seeking behavior and rampant spending on absurd stuff is almost certainly due to reduced inhibitions from the drugs. On the other hand, I don’t understand how someone can have gained so much weight while abusing stimulants. Sheesh, he is a mess.

Very impressive that your post got a trackback from Tyler Cowen the marginal revolutionary!

Until 6 weeks ago, I worked for the 30th largest US bank. I did capital and liquidity risk management. My bank is going straight to hell. The 2-day intern’s account and the sources that came before ring true to my work days (although not nearly as r/acc): Scrambling for sources of liquidity day-to-day (and capital in general) yet no one wants to talk about how bad it is. I think you have captured the FTX/Alameda situation quite well. I wonder if they even had a single CPA on the payroll… that proto-balance sheet screen shot is shocking.

That brings up another thing: Alameda used some BS public accounting company that claimed to provide real-time PoR (yes, that’s Proof of Reserves). They have been retained by other crypto scammers, and recently determined (probably by AutismCapital) to not *really* do what they say they do. I mention this because it provided additional though false confidence for investors in SBF_FTX solvency. Company name is Armanino see here for more about their real-time ‘Trust Explorer’ for PoR https://twitter.com/wheatstones_/status/1544988797875752960

Again, good job reporting!

November 18th, 2022 at 6:13 am

This article is genius!! Thank you

November 18th, 2022 at 3:04 pm

[…] FTX tanked last week (see the Bloomberg columns here and here; also this blog post), philosophers have weighed […]

November 18th, 2022 at 6:21 pm

I was privately giving SBF the benefit of the doubt that he started out decent and then panicked when he ran out of money and *then* crossed the moral boundary of stealing money from FTX depositors.

But it looks like everything was one giant bag of noise from the start. They didn’t even track the stuff they invested in,

November 18th, 2022 at 6:40 pm

Keep in mind Sam wrote his blog from 2016 til 2019, so the fried brain hipotesis doesn’t really work. I wonder if its possible to get through MIT phisics while not being that intelligent.

November 18th, 2022 at 7:16 pm

[…] FTX tanked last week (see the Bloomberg columns here and here; also this blog post), philosophers have weighed […]

November 18th, 2022 at 9:45 pm

There was a real

comment from a ‘trader/ potato. He used a term ‘rekked’

That was cool.

Punters be-ware.

You might be ‘rekked’

Just my personal opinion, channeling the

good

witch of the East. ]

Hold your feet tight inside of them, the magic must be very powerful.

November 18th, 2022 at 9:49 pm

Fantastic article in most respects.

I’m not sold on your claims about SBF being illogical about bet-sizing re: Kelly

(And the related video-game expertise based criticism of his cognition/resulting claims about stimulants frying his brain.)

He says his utility is (close to) linear in dollars.

If you agree with that claim, then I think betting Kelly is indeed worse for you in expectation than betting over Kelly.

Again, he’s claiming to have a very atypical utility function, in claiming his utility is linear in dollars, but I think that given that assumption, his reasoning is fine. (Linearity of expectation says you should just maximize your bet size every time you have a +EV bet.)

You could argue against him having a closer-to-linear utility function than usual businesses, but I think that’s different than the claim you make in your article.

November 18th, 2022 at 10:21 pm

@Kelly: No, the Kelly criterion does not make assumptions about your utility function

November 19th, 2022 at 5:26 am

[…] billion in leveraged funds that didn’t exist while its principle actors were languishing in a drug-infested $40 million villa in the Bahamas even as they preened about the virtues of “effective […]

November 19th, 2022 at 11:39 am

That’s proper investigative journalism. Best summary I’ve read of a complex story, written by someone who knows his way around a trading floor. The drugs angle is interesting, if speculative, since it might explain the disconnect between the fantasy world SBF occupied and the real world. And that’s potentially fatal.

November 19th, 2022 at 6:04 pm

@J Kolpek

Well yes, if you extract one snippet and ignore the context of the entire rest of the blog you can make her look like a moron. The sentiment of the post, however, makes perfect sense and is completely relatable. It’s just written in a casual style. Just as people have treated her obviously somewhat tongue-in-cheek comment about imperial Chinese harem polygamy as showing that her entire life revolved around setting up such a harem or whatever. Or the characterizations of her as a “Harry Potter fan” as though that’s the only content on the blog.

November 19th, 2022 at 7:37 pm

Fast forward to? After he gets out of jail?

After he gets a hand slap and is living in his parents basement?

After he spends enough time at a drug treatment facility ( if he can afford it, if not M&D will pay )?

He receives an honorary title from Stanford and teaches a course on how to run a Ponzi scheme.

He pitches a course for how to successfully manage nootropics as part of your daily regimen; gets turned down, but after a name change substituting nootropics for psychedelics gets approval.

He is reborn and becomes the poster child for the next latest and greatest investment opportunity. Can’t wait for the emotional out pouring of his confessional on 60 minutes.

November 20th, 2022 at 7:24 am

>What could be possibly hope to accomplish with this?

a better court decision

November 20th, 2022 at 8:30 pm

@milkyeggs: Kelly does make assumptions about your utility function.

See finance uber-chad Arthur Brietman on this: https://twitter.com/arthurb/status/1592301625972264961

It should be obvious that Kelly has to make assumptions about your utility function. Suppose you have a fair coin and someone gives you a chance to bet to double your money if you win, and halve it if you lose. Imagine a utility function that prefers the situation where you bet all of your money on this flip. Is this impossible? No — people can have this utility function if they want. Yet Kelly doesn’t bet all the money. So Kelly is making an assumption about your utulity function.

November 21st, 2022 at 2:59 am

where is the Alex Mashinsky case at? He hasn’t seen any jail time.

Jessica Khater, the head of institutional lending was a porn star…nobody batted an eye and thought everything was fine.

Do Kwon isn’t in jail as far as we know.

So what’s going on really? Why don’t these criminals go to jail for committing fraud, are tehy protected? Is it all because a case has to be built against them so they need to be kept safe until trial/are they conspiring with the banks and regulators behind closed doors?

November 21st, 2022 at 12:23 pm

[…] Addendum: Drawing on many excellent sources including Matt Levine, the FT, and Milky Eggs. […]

November 22nd, 2022 at 5:42 am

Хороший анализ!

November 23rd, 2022 at 7:27 am

gen z has zero concept of anything real or meaningful most fucked generation … ever

November 24th, 2022 at 4:56 pm

[…] downfall of FTX attributed due to negligent economic practices, a bad and erratic management style, excessive spending on […]

November 26th, 2022 at 3:11 am

It’s possible that the Kelly bet sizing criterion really does depend on your choice of utility function, even in the case of repeated bets.

Kelly himself says:

“One might still argue that the gambler should bet all his money (make L = 1) in order to maximize his expected win after N times. It is surely true that if the game were to be stopped after N bets the answer to this question would depend on the relative values (to the gambler) of being broke or possessing a fortune. If we compare the fates of two gamblers, however, playing a nonterminating game, the one which uses the value L found above will, with probability one, eventually get ahead and stay ahead of one using any other L.” — Kelly (A New Interpretation of Information Rate, 1956) p. 920. https://www.turtletrader.com/kelly.pdf

Some other papers relating to this issue:

The “Fallacy” of Maximizing the Geometric Mean in Long Sequences of Investing or Gambling

Paul A. Samuelson

https://www.pnas.org/doi/10.1073/pnas.68.10.2493

Psychology is Fundamental: The Limitations of Growth-Optimal Approaches to Decision Making under Uncertainty

Matthew Ford and John Kay

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4140625

November 30th, 2022 at 10:18 pm

sbf just announced that he gave money to republicans as well as dems, how do you think that will effect the investigation and any charges against him?

December 11th, 2022 at 12:23 am

[…] want to thank the blog Milky Eggs for their excellent breakdown on the history of the Death Star. They have done much more in-depth […]

December 11th, 2022 at 2:49 pm

@TheNoticing: Your concerns are the same as mine.Nearly two weeks later, and at least five hours of watching SBF dissemble and say, “I don’t recall” and “I don’t know” like Hillary and Mueller, and I’m beginning to wonder if he will even have a warrant issued for his arrest.

Caroline was very definitively sighted in a Manhattan cappucino-ry last week by AutismCapital loyalists. SBF isn’t going to be easily dislodged from the Bahamas despite what Maxine Waters wants.

@reader I’ve come around to your way of thinking:

@JHE is likely correct about Caroline. Since all that’s known about her is the ridiculous video clip saying she doesn’t use math, and the harem blog post, the focus is on that exclusively. She seems more interesting by far than the blob that is SBF.

@say I am working on the thankless task of the Wikipedia BLP for SBF right now. SBF gave 99% of his Fed Election Campaign donations in 2021-2022 election cycle to Dems and 1% to GOP. However, he says he gave additional funds in dark money (to 501(c)4s I guess) to Dems and GOP in amounts unknown. That’s a good question, about the effect that might have on the investigation, assuming SBF is telling the truth… which he doesn’t do a lot of.

January 11th, 2023 at 4:02 pm

can anyone tell me how you can set up a rss feed to automatically download anime

January 16th, 2023 at 9:47 am

@go white boy go: Yes, think you can just add a Nyaa.si search like https://nyaa.si/?f=0&c=0_0&q=asdf directly as an RSS feed into your torrent client.